factors_r = ["SP500", "DTWEXAFEGS"] # "SP500" does not contain dividends; note: "DTWEXM" discontinued as of Jan 2020

factors_d = ["DGS10", "BAMLH0A0HYM2"]Black-Scholes model

from scipy.stats import normdef level_shock(shock, S, tau, sigma):

result = S * (1 + shock * sigma * np.sqrt(tau))

return result- https://en.wikipedia.org/wiki/Greeks_(finance)

- https://www.wolframalpha.com/input/?i=option+pricing+formula

factor = "SP500"

types = ["call", "put"]

S = levels_df.ffill()[factor].iloc[-1]

K = S

r = 0 # use "USD3MTD156N"

q = 0 # see https://stackoverflow.com/a/11286679

tau = 1 # = 252 / 252

sigma = sd_df[factor].iloc[-1] # use "VIXCLS"

shocks = [x / 2 for x in range(-6, 7)]greeks_df = pd.DataFrame([(x, y) for x in types for y in shocks],

columns = ["type", "shock"])

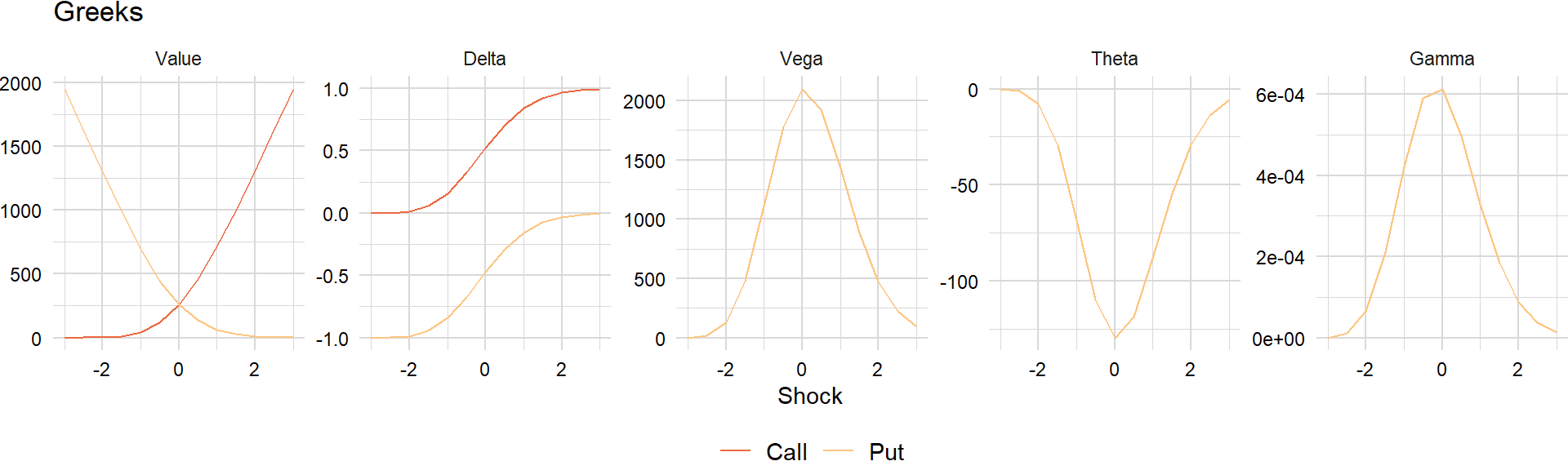

greeks_df["spot"] = level_shock(greeks_df["shock"], S, tau, sigma)Value

For a given spot price \(S\), strike price \(K\), risk-free rate \(r\), annual dividend yield \(q\), time-to-maturity \(\tau = T - t\), and volatility \(\sigma\):

\[ \begin{aligned} V_{c}&=Se^{-q\tau}\Phi(d_{1})-e^{-r\tau}K\Phi(d_{2}) \\ V_{p}&=e^{-r\tau}K\Phi(-d_{2})-Se^{-q\tau}\Phi(-d_{1}) \end{aligned} \]

def bs_value(type, S, K, r, q, tau, sigma, d1, d2):

r_df = np.exp(-r * tau)

q_df = np.exp(-q * tau)

call_value = S * q_df * Phi(d1) - r_df * K * Phi(d2)

put_value = r_df * K * Phi(-d2) - S * q_df * Phi(-d1)

result = np.where(type == "call", call_value, put_value)

return resultwhere

\[ \begin{aligned} d_{1}&={\frac{\ln(S/K)+(r-q+\sigma^{2}/2)\tau}{\sigma{\sqrt{\tau}}}} \\ d_{2}&={\frac{\ln(S/K)+(r-q-\sigma^{2}/2)\tau}{\sigma{\sqrt{\tau}}}}=d_{1}-\sigma{\sqrt{\tau}} \\ \phi(x)&={\frac{e^{-{\frac {x^{2}}{2}}}}{\sqrt{2\pi}}} \\ \Phi(x)&={\frac{1}{\sqrt{2\pi}}}\int_{-\infty}^{x}e^{-{\frac{y^{2}}{2}}}dy=1-{\frac{1}{\sqrt{2\pi}}}\int_{x}^{\infty}e^{-{\frac{y^{2}}{2}}}dy \end{aligned} \]

def bs_d1(S, K, r, q, tau, sigma):

result = (np.log(S / K) + (r - q + sigma ** 2 / 2) * tau) / (sigma * np.sqrt(tau))

return result

def bs_d2(S, K, r, q, tau, sigma):

result = (np.log(S / K) + (r - q - sigma ** 2 / 2) * tau) / (sigma * np.sqrt(tau))

return result

def phi(x):

result = norm.pdf(x)

return result

def Phi(x):

result = norm.cdf(x)

return resultgreeks_df["d1"] = bs_d1(greeks_df["spot"], K, r, q, tau, sigma)

greeks_df["d2"] = bs_d2(greeks_df["spot"], K, r, q, tau, sigma)

greeks_df["value"] = bs_value(greeks_df["type"], greeks_df["spot"], K, r, q, tau, sigma,

greeks_df["d1"], greeks_df["d2"]) First-order

Delta

\[ \begin{aligned} \Delta_{c}&={\frac{\partial V_{c}}{\partial S}}=e^{-q\tau}\Phi(d_{1}) \\ \Delta_{p}&={\frac{\partial V_{p}}{\partial S}}=-e^{-q\tau}\Phi(-d_{1}) \end{aligned} \]

def bs_delta(type, S, K, r, q, tau, sigma, d1, d2):

q_df = np.exp(-q * tau)

call_value = q_df * Phi(d1)

put_value = -q_df * Phi(-d1)

result = np.where(type == "call", call_value, put_value)

return resultgreeks_df["delta"] = bs_delta(greeks_df["type"], greeks_df["spot"], K, r, q, tau, sigma,

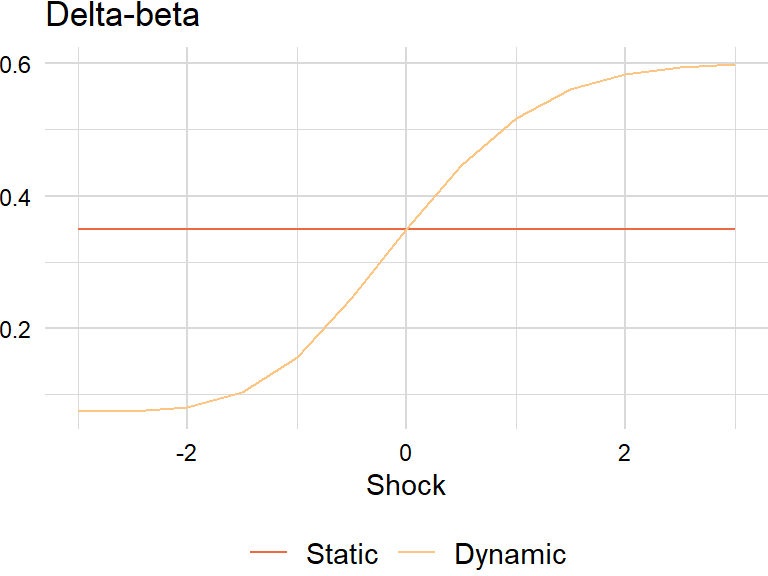

greeks_df["d1"], greeks_df["d2"]) Delta-beta

Notional market value is the market value of a leveraged position:

\[ \begin{aligned} \text{Equity options }=&\,\#\text{ contracts}\times\text{multiple}\times\text{spot price}\\ \text{Delta-adjusted }=&\,\#\text{ contracts}\times\text{multiple}\times\text{spot price}\times\text{delta} \end{aligned} \]

def bs_delta_diff(type, S, K, r, q, tau, sigma, delta0):

d1 = bs_d1(S, K, r, q, tau, sigma)

d2 = bs_d2(S, K, r, q, tau, sigma)

delta = bs_delta(type, S, K, r, q, tau, sigma, d1, d2)

call_value = delta - delta0

put_value = delta0 - delta

result = np.where(type == "call", call_value, put_value)

return resultbeta = 0.35

type = "call"

n = 1

multiple = 100

total = 1000000d1 = bs_d1(S, K, r, q, tau, sigma)

d2 = bs_d2(S, K, r, q, tau, sigma)

sec = {

"n": n,

"multiple": multiple,

"S": S,

"delta": bs_delta(type, S, K, r, q, tau, sigma, d1, d2),

"beta": 1

}beta_df = pd.DataFrame([(type, y) for y in shocks],

columns = ["type", "shock"])

beta_df["spot"] = level_shock(beta_df["shock"], S, tau, sigma)

beta_df["static"] = beta

beta_df["diff"] = bs_delta_diff(type, beta_df["spot"], K, r, q, tau, sigma, sec["delta"])

beta_df["dynamic"] = beta + sec["n"] * sec["multiple"] * sec["S"] * sec["beta"] * beta_df["diff"] / total

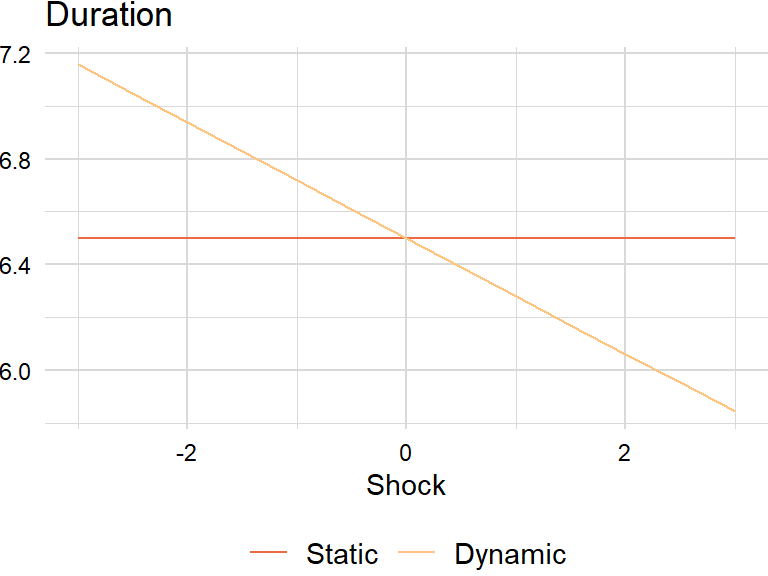

For completeness, duration equivalent is defined as:

\[ \begin{aligned} \text{10-year equivalent }=\,&\frac{\text{security duration}}{\text{10-year OTR duration}} \end{aligned} \]

Vega

\[ \begin{aligned} \nu_{c,p}&={\frac{\partial V_{c,p}}{\partial\sigma}}=Se^{-q\tau}\phi(d_{1}){\sqrt{\tau}}=Ke^{-r\tau}\phi(d_{2}){\sqrt{\tau}} \end{aligned} \]

def bs_vega(type, S, K, r, q, tau, sigma, d1, d2):

q_df = np.exp(-q * tau)

result = S * q_df * phi(d1) * np.sqrt(tau)

return resultgreeks_df["vega"] = bs_vega(greeks_df["type"], greeks_df["spot"], K, r, q, tau, sigma,

greeks_df["d1"], greeks_df["d2"]) Theta

\[ \begin{aligned} \Theta_{c}&=-{\frac{\partial V_{c}}{\partial \tau}}=-e^{-q\tau}{\frac{S\phi(d_{1})\sigma}{2{\sqrt{\tau}}}}-rKe^{-r\tau}\Phi(d_{2})+qSe^{-q\tau}\Phi(d_{1}) \\ \Theta_{p}&=-{\frac{\partial V_{p}}{\partial \tau}}=-e^{-q\tau}{\frac{S\phi(d_{1})\sigma}{2{\sqrt{\tau}}}}+rKe^{-r\tau}\Phi(-d_{2})-qSe^{-q\tau}\Phi(-d_{1}) \end{aligned} \]

def bs_theta(type, S, K, r, q, tau, sigma, d1, d2):

r_df = np.exp(-r * tau)

q_df = np.exp(-q * tau)

call_value = -q_df * S * phi(d1) * sigma / (2 * np.sqrt(tau)) - \

r * K * r_df * Phi(d2) + q * S * q_df * Phi(d1)

put_value = -q_df * S * phi(d1) * sigma / (2 * np.sqrt(tau)) + \

r * K * r_df * Phi(-d2) - q * S * q_df * Phi(-d1)

result = np.where(type == "call", call_value, put_value)

return resultgreeks_df["theta"] = bs_theta(greeks_df["type"], greeks_df["spot"], K, r, q, tau, sigma,

greeks_df["d1"], greeks_df["d2"]) Second-order

Gamma

\[ \begin{aligned} \Gamma_{c,p}&={\frac{\partial\Delta_{c,p}}{\partial S}}={\frac{\partial^{2}V_{c,p}}{\partial S^{2}}}=e^{-q\tau}{\frac{\phi(d_{1})}{S\sigma{\sqrt{\tau}}}}=Ke^{-r\tau}{\frac{\phi(d_{2})}{S^{2}\sigma{\sqrt{\tau}}}} \end{aligned} \]

def bs_gamma(type, S, K, r, q, tau, sigma, d1, d2):

q_df = np.exp(-q * tau)

result = q_df * phi(d1) / (S * sigma * np.sqrt(tau))

return resultgreeks_df["gamma"] = bs_gamma(greeks_df["type"], greeks_df["spot"], K, r, q, tau, sigma,

greeks_df["d1"], greeks_df["d2"])

Taylor series

First-order

Price-yield formula

For a function of one variable, \(f(x)\), the Taylor series formula is:

\[ \begin{aligned} f(x+\Delta x)&=f(x)+{\frac{f'(x)}{1!}}\Delta x+{\frac{f''(x)}{2!}}(\Delta x)^{2}+{\frac{f^{(3)}(x)}{3!}}(\Delta x)^{3}+\cdots+{\frac{f^{(n)}(x)}{n!}}(\Delta x)^{n}+\cdots\\ f(x+\Delta x)-f(x)&={\frac{f'(x)}{1!}}\Delta x+{\frac{f''(x)}{2!}}(\Delta x)^{2}+{\frac{f^{(3)}(x)}{3!}}(\Delta x)^{3}+\cdots+{\frac{f^{(n)}(x)}{n!}}(\Delta x)^{n}+\cdots \end{aligned} \]

Using the price-yield formula, the estimated percentage change in price for a change in yield is:

\[ \begin{aligned} P(y+\Delta y)-P(y)&\approx{\frac{P'(y)}{1!}}\Delta y+{\frac{P''(y)}{2!}}(\Delta y)^{2}\\ &\approx -D\Delta y +{\frac{C}{2!}}(\Delta y)^{2} \end{aligned} \]

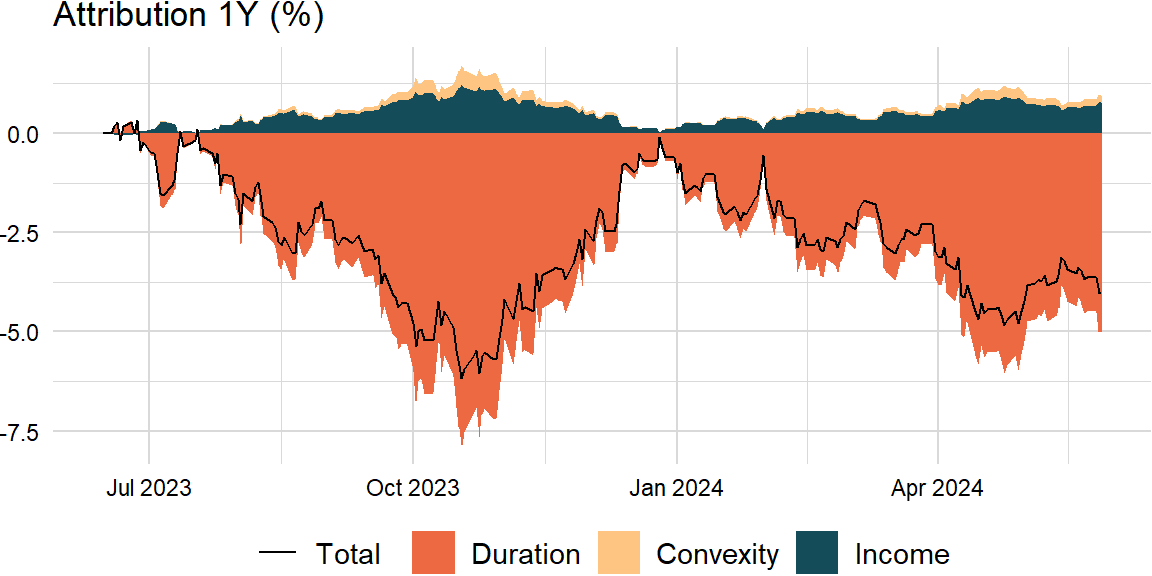

Total return also includes income, i.e. the yield earned over the elapsed time \(y\Delta t\), in addition to the price change:

def pnl_bond(duration, convexity, dy, y, t):

duration_pnl = -duration * dy

convexity_pnl = (convexity * 100 / 2) * dy ** 2

income_pnl = (y / 100) * t

result = pd.DataFrame({

"total": duration_pnl + convexity_pnl + income_pnl,

"duration": duration_pnl,

"convexity": convexity_pnl,

"income": income_pnl

})

return result- https://engineering.nyu.edu/sites/default/files/2021-07/CarWuRF2021.pdf

- https://onlinelibrary.wiley.com/doi/pdf/10.1002/9781118267967.app1

- https://www.investopedia.com/terms/c/convexity-adjustment.asp

factor = "DGS10"

duration = 6.5

convexity = 0.65 # market convention, i.e. 65 / 100 (see duration-yield formula)

y = levels_df.ffill()[factor].iloc[-width]bond_df = pd.DataFrame({

"duration": duration,

"convexity": convexity,

"dy": (levels_df.ffill()[factor].iloc[-width:] - y) / 100,

"t": np.arange(width) / scale["periods"]

})attrib_df = pnl_bond(bond_df["duration"], bond_df["convexity"], bond_df["dy"], y, bond_df["t"])

Duration-yield formula

The derivative of duration with respect to interest rates gives:

\[ \begin{aligned} \text{Drift}&=\frac{\partial D}{\partial y}=\frac{\partial}{\partial y}\left(-\frac{1}{P}\frac{\partial P}{\partial y}\right)\\ &=-\frac{1}{P}\frac{\partial^{2}P}{\partial y^{2}}+\frac{1}{P^{2}}\frac{\partial P}{\partial y}\frac{\partial P}{\partial y}\\ &=-C+D^{2} \end{aligned} \]

Because of market conventions, use the following formula: \(\text{Drift}=\frac{1}{100}\left(-C\times 100+D^{2}\right)=-C+\frac{D^{2}}{100}\). For example, if convexity and yield are percent then \(\text{Drift}=\left(-0.65+\frac{6.5^{2}}{100}\right)\partial y\times100\) or basis points then \(\text{Drift}=\left(-65+6.5^{2}\right)\partial y\).

def yield_shock(shock, tau, sigma):

result = shock * sigma * np.sqrt(tau)

return resultdef duration_drift(duration, convexity, dy):

drift = -convexity + duration ** 2 / 100

change = drift * dy * 100

result = {

"drift": drift,

"change": change

}

return result# "Risk Management: Approaches for Fixed Income Markets" (page 45)

factor = "DGS10"

sigma = sd_df[factor].iloc[-1]duration_df = pd.DataFrame(shocks).rename(columns = {0: "shock"})

duration_df["spot"] = yield_shock(duration_df["shock"], tau, sigma)

duration_df["static"] = duration

duration_df["dynamic"] = duration + \

duration_drift(duration, convexity, duration_df["spot"])["change"]

Second-order

Greeks P&L decomposition

A similar formula holds for functions of several variables \(f(x_{1},\ldots,x_{n})\). This is usually written as:

\[ \begin{aligned} f(x_{1}+\Delta x_{1},\ldots,x_{n}+\Delta x_{n})&=f(x_{1},\ldots, x_{n})+ \sum _{j=1}^{n}{\frac{\partial f(x_{1},\ldots,x_{n})}{\partial x_{j}}}(\Delta x_{j})\\ &+{\frac {1}{2!}}\sum_{j=1}^{n}\sum_{k=1}^{n}{\frac{\partial^{2}f(x_{1},\ldots,x_{d})}{\partial x_{j}\partial x_{k}}}(\Delta x_{j})(\Delta x_{k})+\cdots \end{aligned} \]

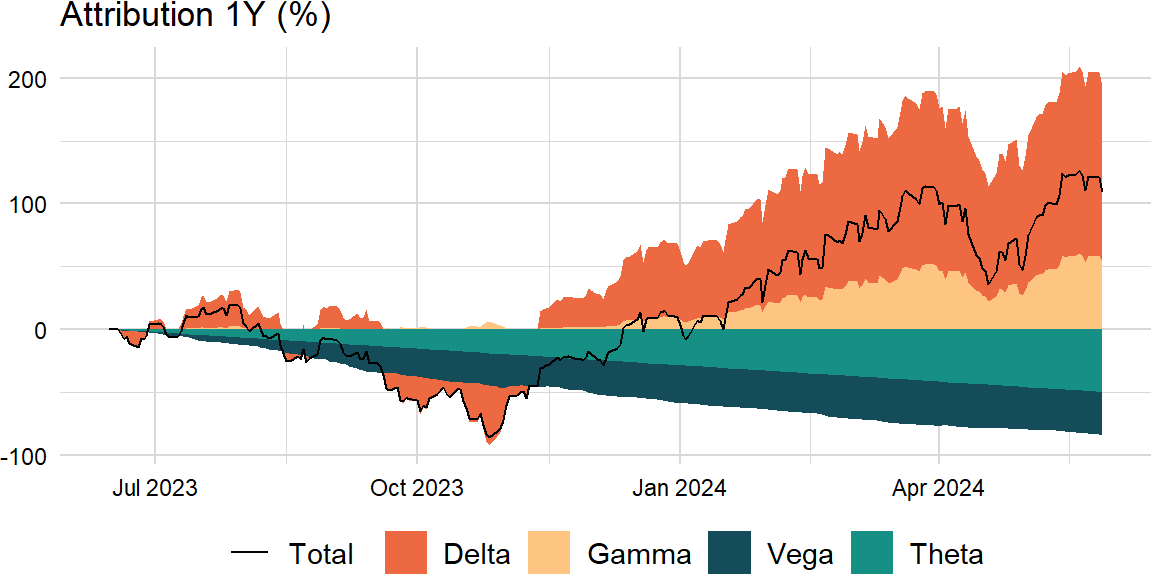

Using the greeks, the estimated change of an option price is:

\[ \begin{aligned} V(S+\Delta S,\sigma+\Delta\sigma,t+\Delta t)-V(S,\sigma,t)&\approx{\frac{\partial V}{\partial S}}\Delta S+{\frac{1}{2!}}{\frac{\partial^{2}V}{\partial S^{2}}}(\Delta S)^{2}+{\frac{\partial V}{\partial \sigma}}\Delta\sigma+{\frac{\partial V}{\partial t}}\Delta t\\ &\approx \Delta_{c,p}\Delta S+{\frac{1}{2!}}\Gamma_{c,p}(\Delta S)^{2}+\nu_{c,p}\Delta\sigma+\Theta_{c,p}\Delta t \end{aligned} \]

def pnl_option(type, S, K, r, q, tau, sigma, dS, dt, dsigma):

d1 = bs_d1(S, K, r, q, tau, sigma)

d2 = bs_d2(S, K, r, q, tau, sigma)

value = bs_value(type, S, K, r, q, tau, sigma, d1, d2)

delta = bs_delta(type, S, K, r, q, tau, sigma, d1, d2)

vega = bs_vega(type, S, K, r, q, tau, sigma, d1, d2)

theta = bs_theta(type, S, K, r, q, tau, sigma, d1, d2)

gamma = bs_gamma(type, S, K, r, q, tau, sigma, d1, d2)

delta_pnl = delta * dS / value

gamma_pnl = gamma / 2 * dS ** 2 / value

vega_pnl = vega * dsigma / value

theta_pnl = theta * dt / value

result = pd.DataFrame({

"total": delta_pnl + gamma_pnl + vega_pnl + theta_pnl,

"delta": delta_pnl,

"gamma": gamma_pnl,

"vega": vega_pnl,

"theta": theta_pnl

})

return resultfactor = "SP500"

type = "call"

S = levels_df.ffill()[factor].iloc[-width]

K = S # * (1 + 0.05)

tau = 1 # = 252 / 252

sigma = sd_df[factor].iloc[-width]options_df = pd.DataFrame({

"spot": levels_df.ffill()[factor].iloc[-width:],

"sigma": sd_df[factor].iloc[-width:]

})

options_df["dS"] = options_df["spot"] - S

options_df["dt_diff"] = (options_df.index - options_df.index[0]).days

options_df["dt"] = options_df["dt_diff"] / options_df["dt_diff"].iloc[-1]

options_df["dsigma"] = options_df["sigma"] - sigmaattrib_df = pnl_option(type, S, K, r, q, tau, sigma,

options_df["dS"], options_df["dt"], options_df["dsigma"])

Ito’s lemma

For a given diffusion \(X(t, \omega)\) driven by:

\[ \begin{aligned} dX_{t}&=\mu_{t}dt+\sigma_{t}dB_{t} \end{aligned} \]

Then proceed with the Taylor series for a function of two variables \(f(t,x)\):

\[ \begin{aligned} df&={\frac{\partial f}{\partial t}}dt+{\frac{\partial f}{\partial x}}dx+{\frac{1}{2}}{\frac{\partial^{2}f}{\partial x^{2}}}dx^{2}\\ &={\frac{\partial f}{\partial t}}dt+{\frac{\partial f}{\partial x}}(\mu_{t}dt+\sigma_{t}dB_{t})+{\frac{1}{2}}{\frac{\partial^{2}f}{\partial x^{2}}}\left(\mu_{t}^{2}dt^{2}+2\mu_{t}\sigma _{t}dtdB_{t}+\sigma_{t}^{2}dB_{t}^{2}\right)\\ &=\left({\frac{\partial f}{\partial t}}+\mu_{t}{\frac{\partial f}{\partial x}}+{\frac{\sigma _{t}^{2}}{2}}{\frac{\partial ^{2}f}{\partial x^{2}}}\right)dt+\sigma_{t}{\frac{\partial f}{\partial x}}dB_{t} \end{aligned} \]

Note: set the \(dt^{2}\) and \(dtdB_{t}\) terms to zero and substitute \(dt\) for \(dB^{2}\).

Geometric Brownian motion

The most common application of Ito’s lemma in finance is to start with the percent change of an asset:

\[ \begin{aligned} \frac{dS}{S}&=\mu_{t}dt+\sigma_{t}dB_{t} \end{aligned} \]

Then apply Ito’s lemma with \(f(S)=\log(S)\):

\[ \begin{aligned} d\log(S)&=f^{\prime}(S)dS+{\frac{1}{2}}f^{\prime\prime}(S)S^{2}\sigma^{2}dt\\ &={\frac {1}{S}}\left(\sigma SdB+\mu Sdt\right)-{\frac{1}{2}}\sigma^{2}dt\\ &=\sigma dB+\left(\mu-{\tfrac{\sigma^{2}}{2}}\right)dt \end{aligned} \]

It follows that:

\[ \begin{aligned} \log(S_{t})-\log(S_{0})=\sigma B_{t}+\left(\mu-{\tfrac{\sigma^{2}}{2}}\right)t \end{aligned} \]

Exponentiating gives the expression for \(S\):

\[ \begin{aligned} S_{t}=S_{0}\exp\left(\sigma B_{t}+\left(\mu-{\tfrac{\sigma^{2}}{2}}\right)t\right) \end{aligned} \]

This provides a recursive procedure for simulating values of \(S\) at \(t_{0}<t_{1}<\cdots<t_{n}\):

\[ \begin{aligned} S(t_{i+1})&=S(t_{i})\exp\left(\sigma\sqrt{t_{i+1}-t_{i}}Z_{i+1}+\left[\mu-{\tfrac{\sigma^{2}}{2}}\right]\left(t_{i+1}-t_{i}\right)\right) \end{aligned} \]

where \(Z_{1},Z_{2},\ldots,Z_{n}\) are independent standard normals.

def sim_gbm(n_sim, S, mu, sigma, dt):

X = sigma * np.sqrt(dt) * np.random.normal(size = n_sim) + (mu - 0.5 * sigma ** 2) * dt

result = S * np.exp(np.cumsum(X))

return resultThis leads to an algorithm for simulating a multidimensional geometric Brownian motion:

\[ \begin{aligned} S_{k}(t_{i+1})&=S_{k}(t_{i})\exp\left(\sqrt{t_{i+1}-t_{i}}\sum_{j=1}^{d}{A_{kj}Z_{i+1,j}}+\left[\mu_{k}-{\tfrac{\sigma_{k}^{2}}{2}}\right]\left(t_{i+1}-t_{i}\right)\right) \end{aligned} \]

where \(A\) is the Cholesky factor of \(\Sigma\), i.e. \(A\) is any matrix for which \(AA^\mathrm{T}=\Sigma\).

def sim_multi_gbm(n_sim, S, mu, sigma, dt):

n_cols = sigma.shape[1]

Z = np.random.normal(size = n_sim * n_cols).reshape((n_sim, n_cols))

X = np.sqrt(dt) * Z @ np.linalg.cholesky(sigma).T + (mu - 0.5 * np.diag(sigma)) * dt

result = S * np.exp(X.cumsum(axis = 0))

return result- https://arxiv.org/pdf/0812.4210.pdf

- https://quant.stackexchange.com/questions/15219/calibration-of-a-gbm-what-should-dt-be

- https://stackoverflow.com/questions/36463227/geometrical-brownian-motion-simulation-in-r

- https://quant.stackexchange.com/questions/25219/simulate-correlated-geometric-brownian-motion-in-the-r-programming-language

- https://quant.stackexchange.com/questions/35194/estimating-the-historical-drift-and-volatility/

S = [1] * len(factors)

sigma = np.cov(returns_df.dropna().T, ddof = 1) * scale["periods"]

mu = np.array(returns_df.dropna().mean()) * scale["periods"]

mu = mu + np.diag(sigma) / 2 # drift

dt = 1 / scale["periods"]levels_sim = sim_gbm(width + 1, S[0], mu[0], np.sqrt(sigma[0, 0]), dt)Then simulate correlated paths and compare the annualized mean and volatility of the simulated returns with the empirical estimates:

mu_ls = []

sigma_ls = []for i in range(10000):

# assumes underlying stock price follows geometric Brownian motion with constant volatility

levels_sim = pd.DataFrame(sim_multi_gbm(width + 1, S, mu, sigma, dt))

returns_sim = np.log(levels_sim).diff()

mu_sim = returns_sim.mean() * scale["periods"]

sigma_sim = returns_sim.std() * np.sqrt(scale["periods"])

mu_ls.append(mu_sim)

sigma_ls.append(sigma_sim)mu_df = pd.DataFrame(mu_ls)

sigma_df = pd.DataFrame(sigma_ls)pd.DataFrame({

"empirical": np.array(returns_df.dropna().mean()) * scale["periods"],

"theoretical": mu_df.mean()

}) empirical theoretical

0 0.175790 0.175406

1 -0.023246 -0.023447

2 0.001332 0.001290

3 0.003636 0.003549pd.DataFrame({

"empirical": np.sqrt(np.diag(sigma)),

"theoretical": sigma_df.mean()

}) empirical theoretical

0 0.151836 0.151581

1 0.056958 0.056875

2 0.008628 0.008619

3 0.011510 0.011495Vasicek model

# assumes interest rates follow mean-reverting process with constant volatilityNewton’s method

Implied volatility

Newton’s method (main idea is also from a Taylor series) is a method for finding approximations to the roots of a function \(f(x)\):

\[ \begin{aligned} x_{n+1}=x_{n}-{\frac{f(x_{n})}{f'(x_{n})}} \end{aligned} \]

To solve \(V(\sigma_{n})-V=0\) for \(\sigma_{n}\), use Newton’s method and repeat until \(\left|V(\sigma_{n})-V\right|<\varepsilon\):

\[ \begin{aligned} \sigma_{n+1}=\sigma_{n}-{\frac{V(\sigma_{n})-V}{V'(\sigma_{n})}} \end{aligned} \]

def implied_vol_newton(params, type, S, K, r, q, tau):

target0 = 0

sigma = params["sigma"]

sigma0 = sigma

while (abs(target0 - params["target"]) > params["tol"]):

d1 = bs_d1(S, K, r, q, tau, sigma0)

d2 = bs_d2(S, K, r, q, tau, sigma0)

target0 = bs_value(type, S, K, r, q, tau, sigma0, d1, d2)

d_target0 = bs_vega(type, S, K, r, q, tau, sigma0, d1, d2)

sigma = sigma0 - (target0 - params["target"]) / d_target0

sigma0 = sigma

return sigma- http://www.aspenres.com/documents/help/userguide/help/bopthelp/bopt2Implied_Volatility_Formula.html

- https://books.google.com/books?id=VLi61POD61IC&pg=PA104

S = levels_df.ffill()[factor].iloc[-1]

K = S # * (1 + 0.05)

sigma = sd_df[factor].iloc[-1] # overrides matrix

start1 = 0.2d1 = bs_d1(S, K, r, q, tau, sigma)

d2 = bs_d2(S, K, r, q, tau, sigma)

target1 = bs_value(type, S, K, r, q, tau, sigma, d1, d2)

params1 = {

"target": target1,

"sigma": start1,

"tol": 1e-4 # np.finfo(float).eps

}implied_vol_newton(params1, type, S, K, r, q, tau) np.float64(0.13126001611714114)Yield-to-maturity

Similarly, solve for the yield that equates the present value of cash flows to the target price, and compute duration and convexity from the first and second derivatives:

def yld_newton(params, cash_flows):

target0 = 0

yld0 = params["cpn"] / params["freq"]

yld = yld0 # assignment to `yield` variable is not possible

while (abs(target0 - params["target"]) > params["tol"]):

target0 = 0

d_target0 = 0

dd_target0 = 0

for i in range(len(cash_flows)):

t = i + 1

# present value of cash flows

target0 += cash_flows[i] / (1 + yld0) ** t

# first derivative of present value of cash flows

d_target0 -= t * cash_flows[i] / (1 + yld0) ** (t + 1) # use t for Macaulay duration

# second derivative of present value of cash flows

dd_target0 -= t * (t + 1) * cash_flows[i] / (1 + yld0) ** (t + 2)

yld = yld0 - (target0 - params["target"]) / d_target0

yld0 = yld

result = {

"price": target0,

"yield": yld * params["freq"],

"duration": -d_target0 / params["target"] / params["freq"],

"convexity": -dd_target0 / params["target"] / params["freq"] ** 2

}

return result- https://www.bloomberg.com/markets/rates-bonds/government-bonds/us

- https://quant.stackexchange.com/a/61025

- https://pages.stern.nyu.edu/~igiddy/spreadsheets/duration-convexity.xls

target2 = 0.9928 * 1000 # present value

start2 = 0.0438 # coupon

cash_flows = [start2 * 1000 / 2] * 10 * 2

cash_flows[-1] += 1000params2 = {

"target": target2,

"cpn": start2,

"freq": 2,

"tol": 1e-4 # np.finfo(float).eps

}yld_newton(params2, cash_flows){'price': 992.8000005704454, 'yield': 0.044700757710159994, 'duration': 8.0165959605043, 'convexity': 76.68109754287481}Optimization

from scipy.optimize import minimize_scalarImplied volatility

If the derivative is unknown, try optimization:

def implied_vol_obj(param, type, S, K, r, q, tau, target):

d1 = bs_d1(S, K, r, q, tau, param)

d2 = bs_d2(S, K, r, q, tau, param)

target0 = bs_value(type, S, K, r, q, tau, param, d1, d2)

result = abs(target0 - target)

return result

def implied_vol_optim(param, type, S, K, r, q, tau, target):

result = minimize_scalar(implied_vol_obj, args = (type, S, K, r, q, tau, target),

method = "bounded", bounds = (0, 1))

return np.float64(result.x)implied_vol_optim(start1, type, S, K, r, q, tau, target1)np.float64(0.13126208740942913)Yield-to-maturity

Similarly, solve for the yield-to-maturity using optimization:

def yld_obj(param, cash_flows, target):

target0 = 0

for i in range(len(cash_flows)):

target0 += cash_flows[i] / (1 + param) ** (i + 1)

result = abs(target0 - target)

return result

def yld_optim(params, cash_flows, target):

result = minimize_scalar(yld_obj, args = (cash_flows, target),

method = "bounded", bounds = (0, 1))

return np.float64(result.x) * params["freq"]yld_optim(params2, cash_flows, target2)np.float64(0.04470128206802046)