factors_r = ["SP500", "DTWEXAFEGS"] # "SP500" does not contain dividends; note: "DTWEXM" discontinued as of Jan 2020

factors_d = ["DGS10", "BAMLH0A0HYM2"]Decomposition

Underlying returns are structural bets that can be analyzed through dimension reduction techniques such as principal component analysis (PCA). Most empirical studies apply PCA to a covariance matrix (note: for multi-asset portfolios, the correlation matrix is often used instead because asset-class variances are on different scales) of equity returns (yield changes) and find that movements in the equity markets (yield curve) can be explained by a subset of principal components. For example, the first three principal components of the yield curve can be interpreted as shift, twist, and butterfly, respectively.

\[ \begin{aligned} \boldsymbol{\Sigma}&=\lambda_{1}\mathbf{v}_{1}\mathbf{v}_{1}^\mathrm{T}+\lambda_{2}\mathbf{v}_{2}\mathbf{v}_{2}^\mathrm{T}+\cdots+\lambda_{k}\mathbf{v}_{k}\mathbf{v}_{k}^\mathrm{T}\\ &=V\Lambda V^\mathrm{T} \end{aligned} \]

def eigen(x):

L, V = np.linalg.eigh(np.cov(x.T, ddof = 1))

L = L[::-1]

V = V[:, ::-1]

result = {

"values": L,

"vectors": V

}

return resultdef eigen_decomp(x, comps):

LV = eigen(x)

L = LV["values"][:comps]

V = LV["vectors"][:, :comps]

result = np.dot(V, np.multiply(L[:, None], V.T))

return resultcomps = 1eigen_decomp(overlap_df, comps) * scale["periods"] * scale["overlap"]array([[ 2.32143149e-02, -1.75348441e-03, 1.89937448e-04,

1.31483513e-03],

[-1.75348441e-03, 1.32448775e-04, -1.43468526e-05,

-9.93155694e-05],

[ 1.89937448e-04, -1.43468526e-05, 1.55405121e-06,

1.07578634e-05],

[ 1.31483513e-03, -9.93155694e-05, 1.07578634e-05,

7.44709213e-05]])# np.cov(overlap_df.T) * scale["periods"] * scale["overlap"]Variance

We often look at the proportion of variance explained by the first \(i\) principal components as an indication of how many components are needed.

\[ \begin{aligned} \frac{\sum_{j=1}^{i}{\lambda_{j}}}{\sum_{j=1}^{k}{\lambda_{j}}} \end{aligned} \]

def variance_explained(x):

LV = eigen(x)

L = LV["values"]

result = L.cumsum() / L.sum()

return resultvariance_explained(overlap_df)array([0.87179181, 0.99496842, 0.99799922, 1. ])Similarity

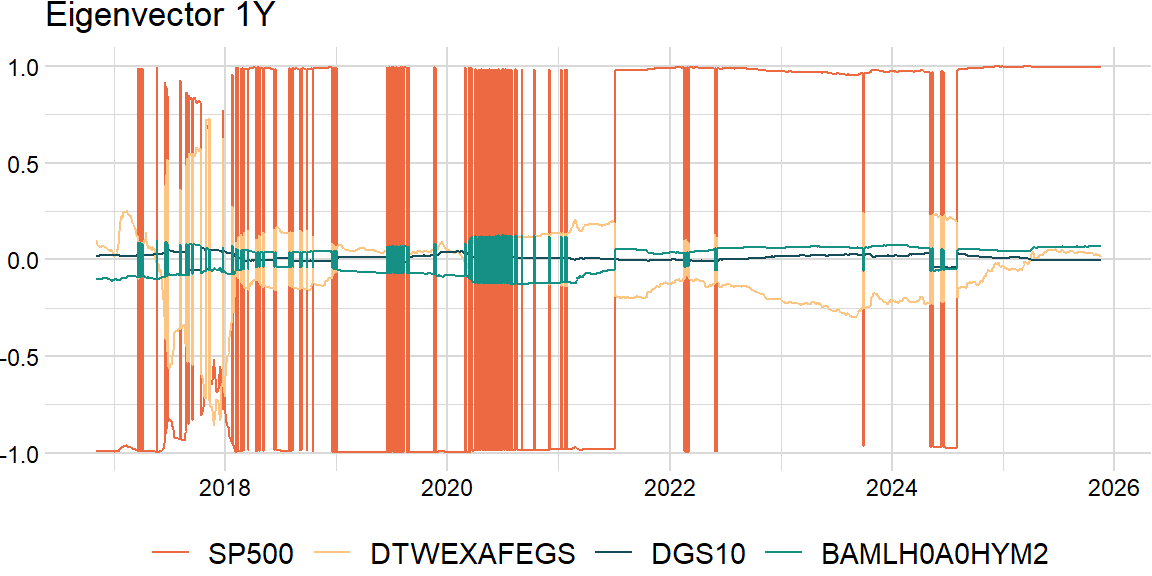

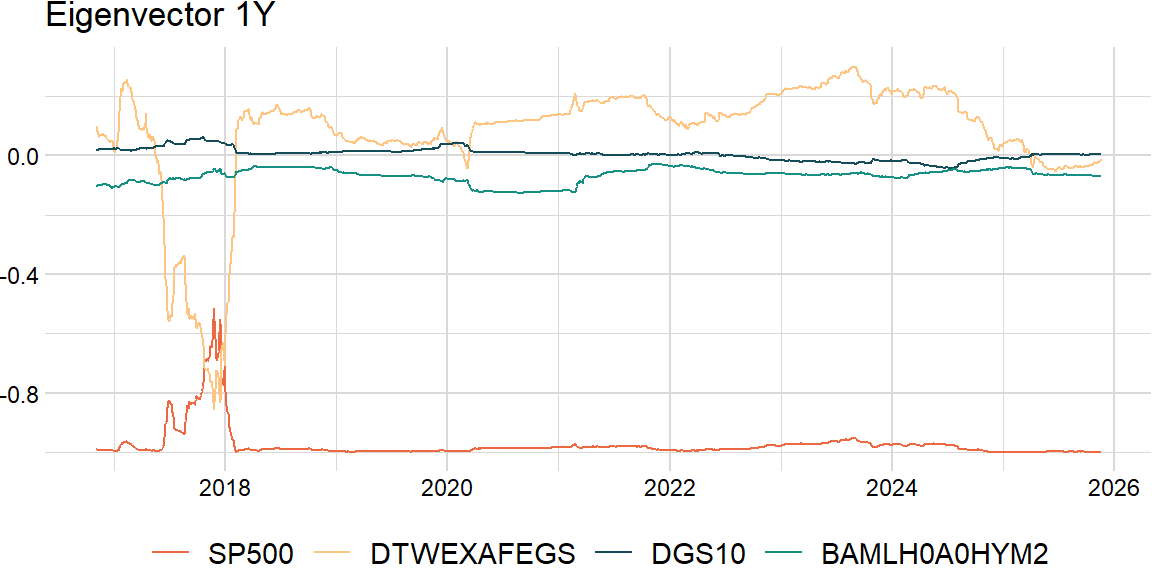

Also, a challenge of rolling PCA is to try to match the eigenvectors: may need to change the sign and order.

\[ \begin{aligned} \text{similarity}=\frac{\mathbf{v}_{t}\cdot\mathbf{v}_{t-1}}{\|\mathbf{v}_{t}\|\|\mathbf{v}_{t-1}\|} \end{aligned} \]

def similarity(V, V0):

n_cols_v = V.shape[1]

n_cols_v0 = V0.shape[1]

result = np.zeros((n_cols_v, n_cols_v0))

for i in range(n_cols_v):

for j in range(n_cols_v0):

result[i, j] = np.dot(V[:, i], V0[:, j]) / \

np.sqrt(np.dot(V[:, i], V[:, i]) * np.dot(V0[:, j], V0[:, j]))

return resultdef roll_eigen1(x, width, comp):

n_rows = len(x)

result_ls = []

for i in range(width - 1, n_rows):

idx = range(max(i - width + 1, 0), i + 1)

LV = eigen(x.iloc[idx])

V = LV["vectors"]

result_ls.append(V[:, comp - 1])

result_df = pd.DataFrame(result_ls, index = x.index[(width - 1):],

columns = x.columns)

return result_df comp = 1raw_df = roll_eigen1(overlap_df, width, comp)

def roll_eigen2(x, width, comp):

n_rows = len(x)

V_ls = []

result_ls = []

for i in range(width - 1, n_rows):

idx = range(max(i - width + 1, 0), i + 1)

LV = eigen(x.iloc[idx])

V = LV["vectors"]

if i > width - 1:

# cosine = np.dot(V.T, V_ls[-1])

cosine = similarity(V, V_ls[-1])

order = np.argmax(np.abs(cosine), axis = 0) # assumes a one-to-one match between windows

V = np.sign(np.diag(cosine[order, :])) * V[:, order]

V_ls.append(V)

result_ls.append(V[:, comp - 1])

result_df = pd.DataFrame(result_ls, index = x.index[(width - 1):],

columns = x.columns)

return result_dfclean_df = roll_eigen2(overlap_df, width, comp)

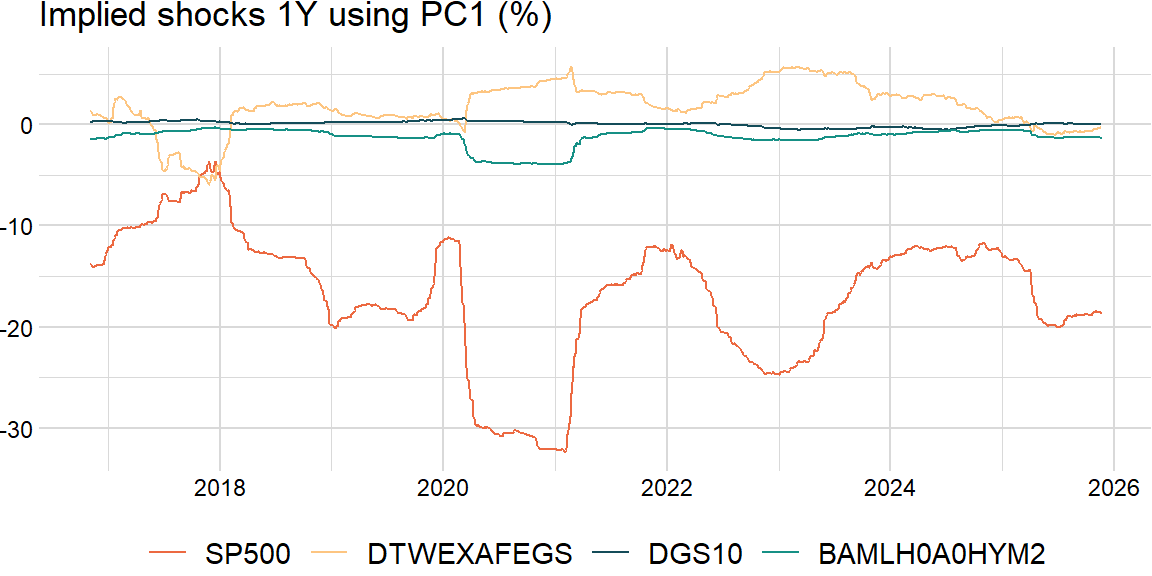

Implied shocks

Implied shocks are the product of the \(n\)th eigenvector and the square root of the \(n\)th eigenvalue (annualized using the square root of time):

\[ \begin{aligned} \sqrt{\lambda_{n}}\mathbf{v}_{n} \end{aligned} \]

def roll_shocks(x, width, comp):

n_rows = len(x)

V_ls = []

result_ls = []

for i in range(width - 1, n_rows):

idx = range(max(i - width + 1, 0), i + 1)

LV = eigen(x.iloc[idx])

L = LV["values"]

V = LV["vectors"]

if i > width - 1:

# cosine = np.dot(V.T, V_ls[-1])

cosine = similarity(V, V_ls[-1])

order = np.argmax(np.abs(cosine), axis = 0) # assumes a one-to-one match between windows

L = L[order]

V = np.sign(np.diag(cosine[order, :])) * V[:, order]

shocks = np.sqrt(L[comp - 1]) * V[:, comp - 1]

V_ls.append(V)

result_ls.append(shocks)

result_df = pd.DataFrame(result_ls, index = x.index[(width - 1):],

columns = x.columns)

return result_dfshocks_df = roll_shocks(overlap_df, width, comp) * np.sqrt(scale["periods"] * scale["overlap"])